Financial Stability Should Begin at Age 7: 7 Money Lessons Every Child Should Learn

Financial stability is one of the most important foundations for a successful and stress-free life. Unfortunately, many adults struggle with debt, overspending, poor saving habits, and a lack of financial planning because they were never taught how money works during childhood.

Just as children learn language, mathematics, and social skills at a young age, they should also learn how to manage money. Financial education does not need to be complicated. In fact, some of the most valuable money lessons can begin as early as age seven.

Children who develop healthy financial habits early are more likely to become financially responsible adults. Here are seven essential financial lessons every child should learn.

1. Understand the Difference Between Needs and Wants

The first step toward financial literacy is understanding the difference between needs and wants.

Needs are things required for living and well-being, such as food, education, healthcare, and clothing. Wants are things that make life enjoyable but are not necessary, such as toys, video games, or luxury items.

Teaching children to identify needs and wants helps them make better spending decisions. When children understand this concept, they begin to think critically before asking for or purchasing something.

This simple lesson forms the foundation for responsible financial behavior throughout life.

2. Learn the Habit of Saving Money

Saving money is one of the most important habits a child can develop.

A piggy bank or savings jar is often the first financial tool children use. Parents can encourage children to save a portion of their pocket money, gifts, or rewards.

Saving teaches patience and discipline. It also helps children understand that money can grow over time when it is not spent immediately.

Small savings habits developed during childhood often become lifelong financial practices that contribute to long-term financial security.

3. Practice Delayed Gratification

We live in a world of instant purchases and instant rewards. However, one of the strongest predictors of future financial success is the ability to delay gratification.

Children should learn that they do not always have to get what they want immediately.

For example, if a child wants a bicycle or a new toy, encourage them to save toward that goal. Waiting and working toward something teaches patience, planning, and self-control.

These qualities help people avoid impulsive purchases and make smarter financial decisions later in life.

4. Learn Basic Budgeting Skills

Budgeting is simply giving every rupee a purpose.

Children can be introduced to budgeting through a simple system:

- Save some money

- Spend some money

- Share some money

For example, if a child receives ₹100, they can allocate ₹50 to savings, ₹30 to spending, and ₹20 to helping others or donating.

This approach teaches financial responsibility while helping children understand that money should be managed rather than spent without thought.

5. Understand the Value of Work

Children should understand that money comes from effort, skills, and productivity.

When children learn the connection between work and earnings, they develop greater appreciation for money and the effort required to earn it.

Simple activities such as helping with age-appropriate responsibilities, participating in small projects, or earning rewards through effort can reinforce this lesson.

Understanding the value of work encourages responsibility, discipline, and respect for resources.

6. Set Financial Goals

Goal-based saving teaches children how to plan for the future.

Instead of spending money randomly, children can save toward specific goals such as books, bicycles, sports equipment, educational kits, or hobbies.

Setting goals gives children motivation and helps them understand the relationship between planning and achievement.

Goal-setting also introduces the concept of long-term thinking, an essential skill for wealth creation and financial success.

7. Avoid Wasteful Spending

Learning how to avoid waste is just as important as learning how to save.

Children should be encouraged to take care of their belongings, avoid unnecessary purchases, and think carefully before spending money.

This lesson helps develop mindfulness and responsible consumption habits.

People who learn to avoid waste during childhood often become adults who manage their finances more effectively and make thoughtful purchasing decisions.

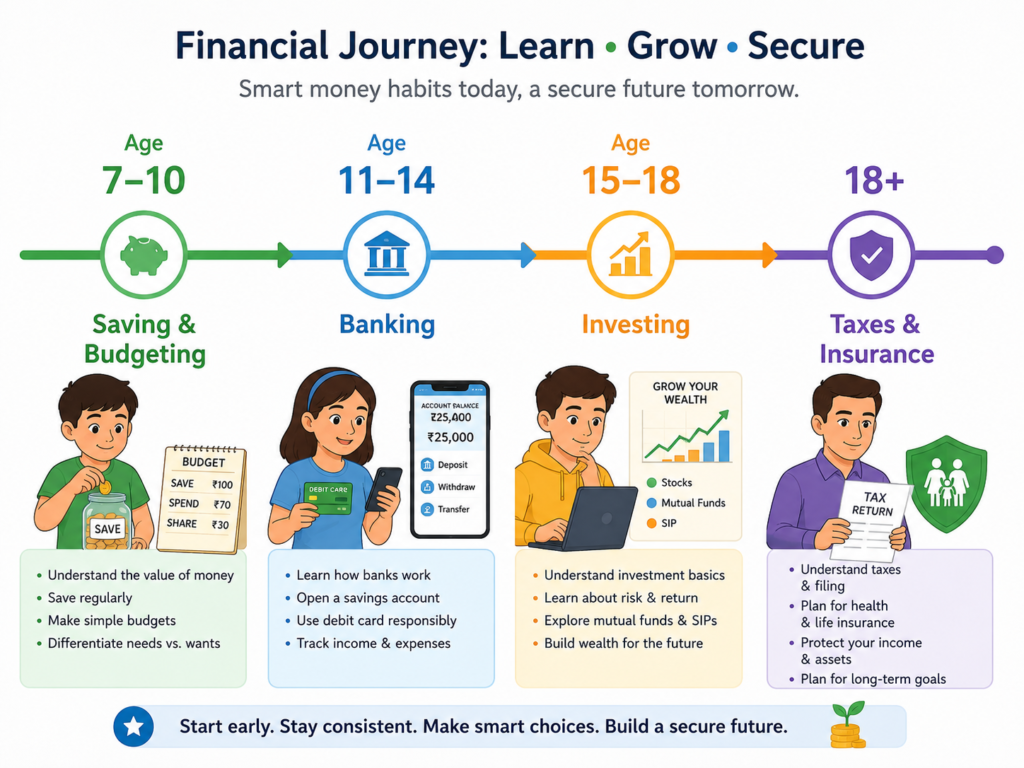

A Financial Education Roadmap for Children

Financial education should evolve as children grow:

Ages 7–10

- Saving money

- Needs vs wants

- Basic budgeting

- Value of money

Ages 11–14

- Banking basics

- Interest and savings accounts

- Smart spending habits

- Digital payments

Ages 15–18

- Investing fundamentals

- Entrepreneurship

- Income generation

- Financial goal planning

Age 18 and Above

- Taxes

- Insurance

- Loans and credit

- Retirement planning

- Wealth creation strategies

Why Early Financial Education Matters

Financial education provides benefits that extend far beyond money.

Children who understand financial concepts often become:

- Better decision-makers

- More disciplined individuals

- Responsible consumers

- Confident problem solvers

- Future investors and entrepreneurs

Most importantly, they are better equipped to avoid debt, manage income wisely, and build long-term financial security.

Conclusion

Schools teach children how to earn a living, but financial education teaches them how to manage and grow their money. The earlier children learn financial literacy, the stronger their financial foundation becomes.

By introducing simple lessons about saving, budgeting, goal-setting, delayed gratification, and responsible spending at age seven, parents and educators can help create a generation that is financially confident and prepared for the future.

Financial stability does not start with a high salary—it starts with smart habits learned in childhood.